Feb 16 – Welcome to the home for real-time coverage of markets brought to you by Reuters reporters. You can share your thoughts with us at markets.research@thomsonreuters.com

INVESTORS UNSUBSCRIBE FROM VIDEO STREAMING STOCKS (1210 EST/1710 GMT)

Investors are ditching video streaming stocks on Wednesday, with ViacomCBS slumping 22% after the media company’s quarterly profits missed analysts’ estimates.

Register now for FREE unlimited access to Reuters.com

Shares of the conglomerate that owns CBS, Showtime, Comedy Central, and MTV were by far the worst performer in the S&P 500.

As well as posting disappointing quarterly results, ViacomCBS announced it will change its name to Paramount, and it announced a large slate of programming – and spending – to help draw new online customers who have several options from Netflix Inc , to Walt Disney Co (DIS.N) and others. read more

With competition continuing to heat up in the streaming space, Netflix is off almost 4% and Discovery Inc (DISCA.O) is losing almost 5%. Walt Disney (DIS.N) is up 0.5% after dipping about 0.7% earlier in the session.

Meanwhile, AMC Networks (AMCX.O) is tumbling 18%, even after the entertainment company reported quarterly revenue and adjusted earnings per share above Wall Street estimates, according to Refinitiv.

Netflix’s stock is now down 35% year to date, having given up practically all of its massive gains from the “work from home” market rally in 2020 and 2021.

(Noel Randewich)

*****

TOO HOT NOT TO COOL DOWN: WEDNESDAY DATA POINTS TO AGGRESSIVE FED TIGHTENING (1127 EST/1527 GMT)

An avalanche of data on Wednesday buried market participants under a pile of evidence that the economy is running hot enough for Powell & Co to toss a bucket of water on it in the form of impending interest rate hikes.

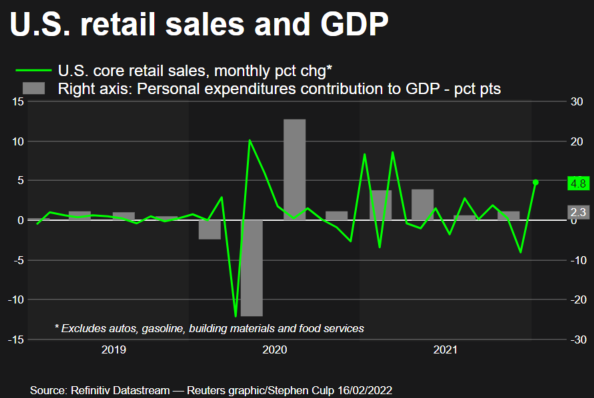

Receipts at U.S. retailers (USRSL=ECI) jumped by 3.8% in January, breezing past the 2% consensus, according to the Commerce Department, rebounding from December’s downwardly revised 2.5% drop. read more

Line-by-line, the clear outlier was non-store retail sales, a category that includes e-commerce, shot up 14.5%. This, combined with a 5.7% jump in autos/parts, more than offset declines in gasoline and food services receipts.

“The strong, broad-based rebound in retail sales after the weak December is particularly impressive given the drag from the Omicron variant and serves as a reminder that the U.S. consumer doesn’t stay down for long,” writes Jeff Buchbinder, equity strategist at LPL Financial.

“Rising wages are supporting spending despite high inflation,” Buchbinder adds.

So-called “core” retail sales, which excludes building materials, autos/parts, gasoline and food services – the measure corresponding most closely tracks the consumer spending element of GDP – jumped 4.8%, well above the more modest 1% gain analysts expected.

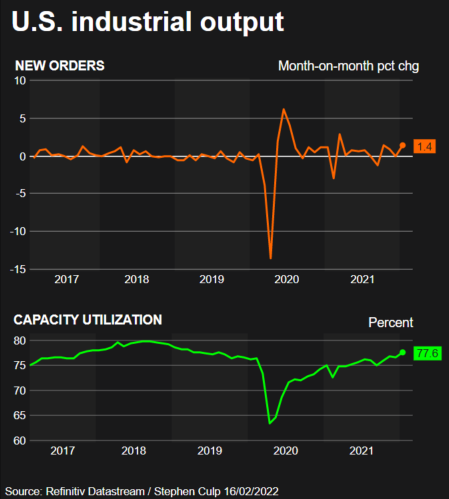

In a separate report, industrial production (USIP=ECI) bounced back more strongly than anticipated in the first weeks of 2022.

Output jumped 1.4% versus the meager 0.4% growth expected, reversing December’s 0.1% dip.

But utilities, amid frigid winter temperatures, did much of the heavy lifting, notes Ian Shepherdson, chief economist at Pantheon Macroeconomics.

“Headline production was hugely flattered by weather effects; colder-than-usual temperatures, both in absolute terms and relative to December, triggered a huge increase in demand for utility energy,” Shepherdson says.

Capacity utilization (USCAPU=ECI), a measure of economic slack, jumped 1.1 percentage points to 77.6%, above the 76.3% pre-pandemic level.

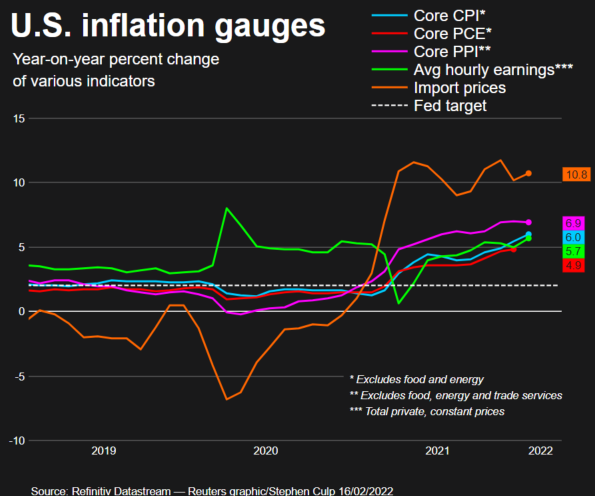

Speaking of supply chain disruptions, let’s talk about inflation. Recent indicators (CPI, PPI, wage growth) have been coming in hotter than anticipated, adding to the probability that the Federal Reserve will take action at its next monetary policy meeting and raise key interest rates.

And the cost of goods imported to the United States (USIMP=ECI), which jumped by 2% in January – the biggest jump in nearly 11 years and above the more tame 1.3% gain expected. read more

Year-over-year, import prices rose a whopping 10.8%, and excluding fuel, hit 6.9% – an all-time high.

“The record pace of core inflation is especially noteworthy as it offers another sign that price pressures are continuing to broaden across the economy in early 2022,” says Mahir Rashid, U.S. economist at Oxford Economics (OE).

The graphic below shows import prices, among other indicators, and how far they continue to soar beyond the Powell & Co’s average annual 2% inflation target:

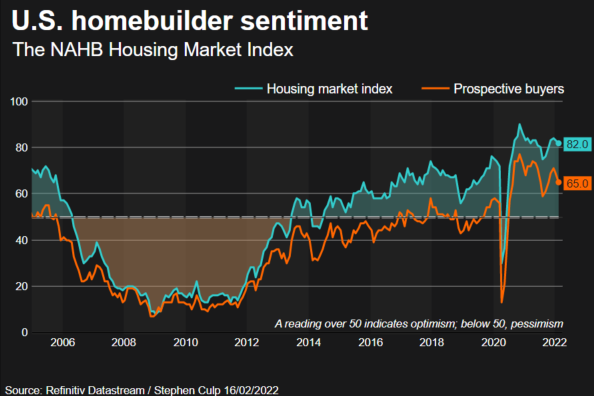

Turning to the housing market, the mood of U.S. homebuilders has dimmed a bit this month.

The National Association of Home Builders’ (NAHB) housing market index (USNAHB=ECI) unexpectedly shed 1 point to a reading of 82. Analysts thought the reading would hold steady.

An NAHB number above 50 signifies optimism.

Waning affordability appears to be weighing on the sector, according to NAHB.

“Rising home prices and interest rates are taking a terrible toll on housing affordability, with 87.5 million households — or roughly 69% of all U.S. households — unable to afford a new median priced home,” they warn on their website.

“Higher input costs and shortages remain headwinds for builders,” says Rubeela Farooqi, chief U.S. economist at High Frequency Economics. “While tight inventories should be supportive of building activity, high prices as well as rising mortgage rates this year will likely be constraints for buyers.”

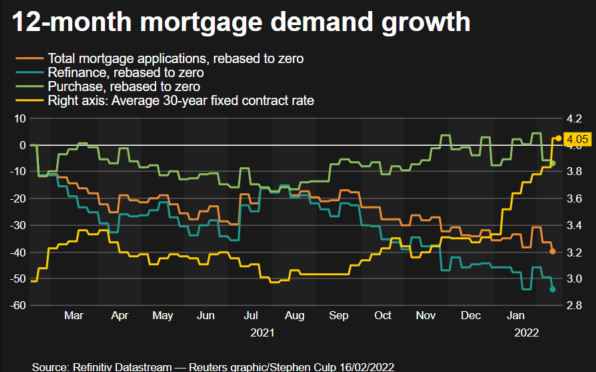

Thanks for the tidy segue, Ms. Farooqi. Demand for home loans dipped last week as interest rates continue their uphill climb, according to the Mortgage Bankers Association (MBA).

The average 30-year fixed contract rate (USMG=ECI) jumped 23 basis points to 4.05%, poking its head above the 4% line for the first time since November 2019.

Applications for loans to purchase homes (USMGPI=ECI) and refinance existing mortgages (USMGR=ECI) both decreased, by 1.2% and 8.9%, respectively.

“The jump in mortgage rates reflected both the backup in Treasury yields and a further widening in mortgage spreads to Treasuries,” says Nancy Vanden Houten, lead economist at OE. “The rise in rates is taking a toll on homebuying affordability and will weigh on home sales in the months ahead.”

The graphic below tells the tale. Total mortgage demand is down 39.8% from the same week last year:

Finally, in more ancient news, the value of goods in the store rooms of U.S. businesses (USBINV=ECI) grew by 2.1% in December, inline with economist forecasts.

The Commerce Department’s inventories seems to confirm its initial take on fourth-quarter GDP, which showed private inventories contributing 4.9 percentage points to the total 6.9% quarterly annualized growth reported late last month.

The mood on Wall Street is sour ahead of the Fed minutes and as investors keep an eye on the constantly shifting situation along the Russia-Ukraine border.

(Stephen Culp)

*****

JITTERS RETURN FOR U.S. STOCKS (0951 EST/1451 GMT)

U.S. stocks are lower in early trade on Wednesday after stronger-than-expected retail sales data gave the Federal Reserve more ammunition to tighten policy, while geopolitical tensions over Russia and Ukraine added to caution.

The data comes ahead of minutes from the Fed’s last meeting, due at 2 p.m. EST. Investors are looking for more clues on the central bank’s plans to trim its massive balance sheet and hike interest rates. read more

In any event, the S&P 500 (.SPX) is finding its 200-day moving average, which now resides around 4,456, to be a sticky level. Traders will be watching to see if the benchmark index can decisively move way from it, in one direction or the other.

Here is where markets stand in early trade:

(Terence Gabriel)

*****

NASDAQ 100 TRIPLE-Qs: CHECKING A FLOW METER (0900 EST/1400 GMT)

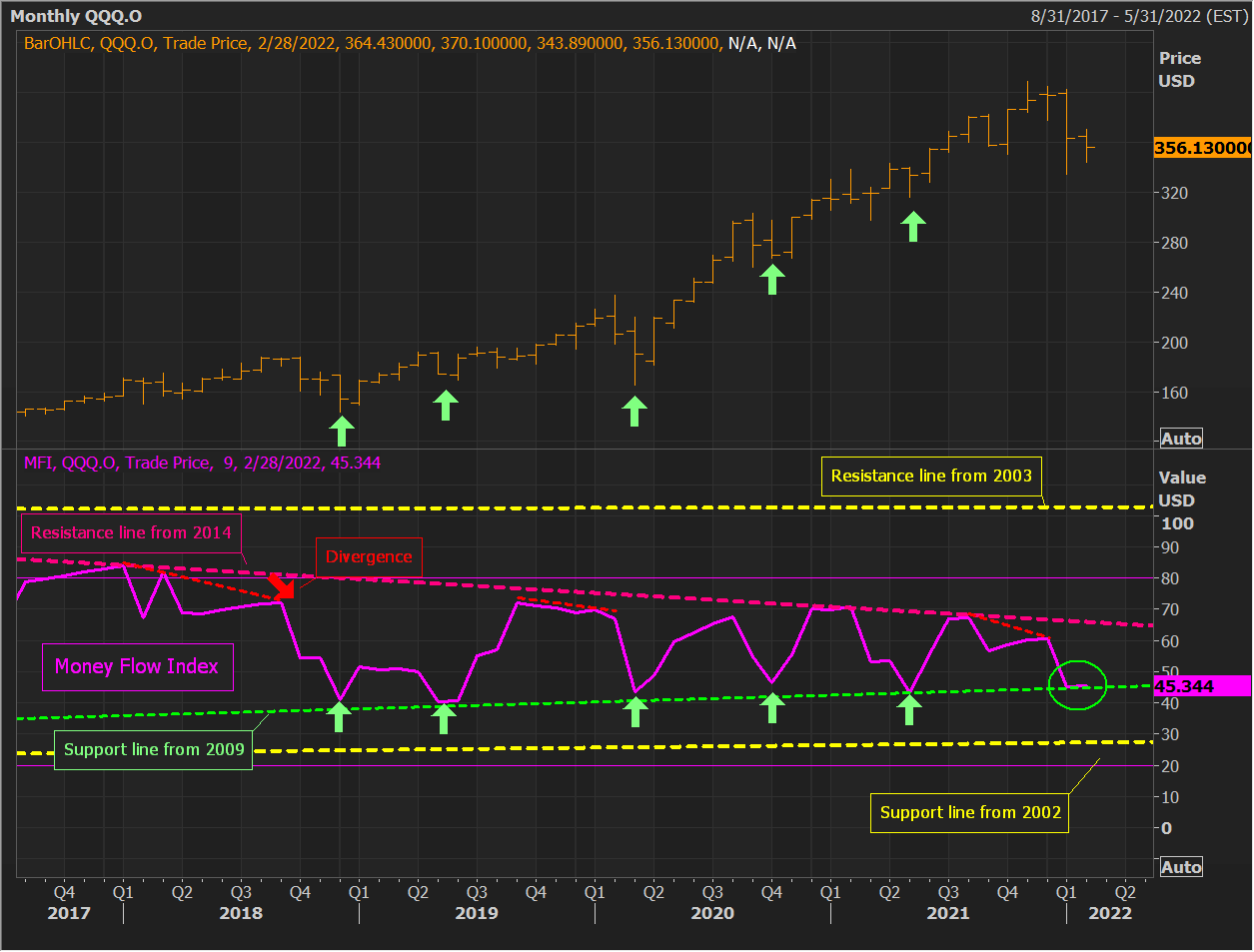

The Invesco QQQ Trust Series 1 (QQQ.O), which tracks the Nasdaq 100 index (.NDX), has been battered of late. That said, the Money Flow index (MFI), an indicator that incorporates both price and volume, is attempting to stabilize at an important support line.

Indeed, the QQQ ended Tuesday down around 12% from its November record close. For 2022, the ETF is off 10.5% so far, and 1.9% this month.

Of note, on a monthly basis, and since early 2018, the MFI has been trapped between a resistance line from its 2014 high and a support line from its 2009 low read more :

After topping shy of the resistance line this past December, while diverging from the QQQ, the MFI plunged in January to once again test the support line. It ended the month essentially right on the line.

So far in February, and despite the QQQ’s monthly drop, the MFI is holding the line, and is actually on track to tick up very slightly.

It is only mid-month, but if the support line can continue to work its magic, and the MFI has bottomed, the QQQ could be on the verge of a surprise upside turn.

Conversely, an MFI support line break at the close of the month will end what has been a consistent pattern. This could then suggest potential that the QQQ could see another waterfall slide given the substantial room before the MFI would reach its support line from 2002. read more

(Terence Gabriel)

*****

FOR WEDNESDAY’S LIVE MARKETS’ POSTS PRIOR TO 0900 EST/1400 GMT – CLICK HERE: read more

Register now for FREE unlimited access to Reuters.com

Terence Gabriel is a Reuters market analyst. The views expressed are his own

Our Standards: The Thomson Reuters Trust Principles.