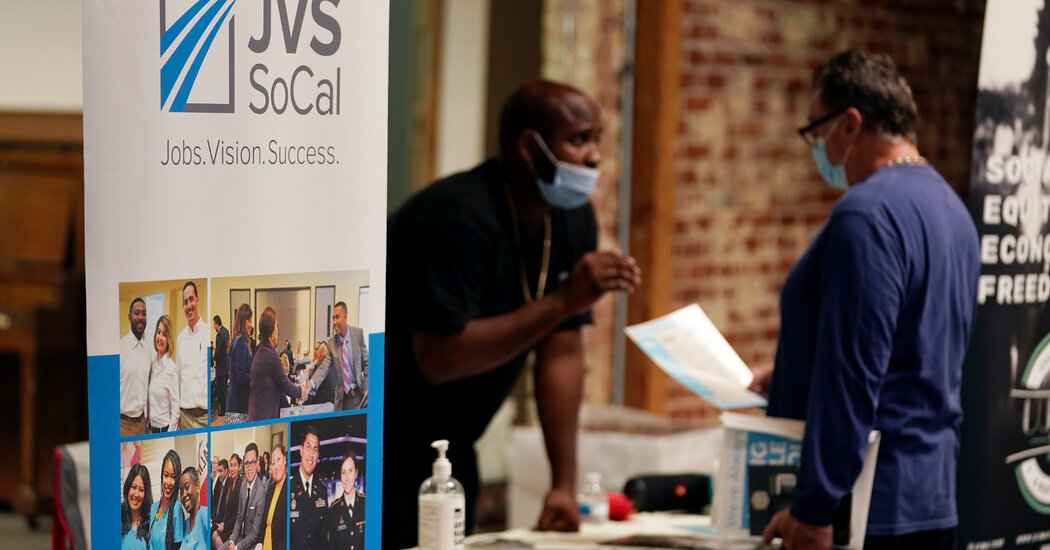

The American economy hit a speed bump in November as hiring unexpectedly dipped before the holiday season, a sign that companies are cautious about prospects for growth.

Employers added 210,000 jobs last month on a seasonally adjusted basis, the Labor Department reported Friday, well below the half-million gain that had been expected. While the data was collected well before the Omicron variant emerged, the figures underscore the economy’s fragility as the pandemic persists.

Despite the weaker-than-expected number for job growth — economists had expected a second straight gain of more than 500,000 — the unemployment rate fell to 4.2 percent from 4.6 percent.

The monthly report from the Bureau of Labor Statistics is based on two separate surveys, one polling households and the other recording hiring among employers. As is the case from time to time, the two surveys painted somewhat different pictures of the economy.

While the data from employers was weaker than forecast, the household survey showed the number of employed Americans jumped by more than 1.1 million. And the participation rate, which measures the proportion of Americans who either have jobs or are looking for one, rose by 0.2 percentage point to 61.8 percent.

Still, the lackluster hiring number was a reminder of the on-again, off-again pattern in the labor market since the pandemic began nearly two years ago.

Throughout the fall, the economy’s path has been characterized by clashing signals.

The “quits rate” — a measurement of workers leaving jobs as a share of overall employment — has been at or near record highs, which suggests that workers are confident they can navigate the labor market to find something better. But the University of Michigan’s survey of consumer sentiment dropped to levels not seen since the sluggish recovery from the recession of 2007-9.

The report noted “the growing belief among consumers that no effective policies have yet been developed to reduce the damage from surging inflation.” Shoppers are facing the steepest inflation in 31 years. In October, prices increased 6.2 percent from a year earlier.

Nonetheless, markets remain relatively calm. The major stock indexes are up by impressive levels this year. And bond yields, which tend to move higher in inflationary environments, remain near record lows, indicating that investors don’t see inflation as a longer-term threat to the economy or financial stability.

In recent days, the chair of the Federal Reserve, Jerome H. Powell, has faced pressure from different political camps to focus more tightly on price increases.

Critics of the Fed say the central bank’s “accommodative” bond-buying policies — which have kept borrowing costs low and led to a large and continued increase in the money supply — went on too long and were irresponsible in light of an already aggressive emergency response from Congress. With inflation proving more stubborn than many experts expected, that suite of stimulative monetary policies is now, in the view of Fed detractors, a prime culprit.

Fed officials, including Mr. Powell, still maintain that the price increases mainly reflect pandemic aberrations that will dissipate. But in congressional testimony on Tuesday, Mr. Powell signaled a pivot from revitalizing the economy to keeping a lid on prices.

“The economy is very strong, and inflationary pressures are high,” he said. “It is therefore appropriate in my view to consider wrapping up the taper of our asset purchases.”

Economists are divided over the potential impact of a winter coronavirus surge. Some say it could cool off the economy, easing inflation, because it could inhibit in-person activities. Others say a new wave could raise prices further by complicating the logistics of supply chains.

John C. Williams, president of the Federal Reserve Bank of New York, told The New York Times on Wednesday that the new variant could “mean a somewhat slower rebound overall” yet “increase those inflationary pressures, in those areas that are in high demand.”

For consumers, one potentially positive effect of renewed virus fears is the recent pullback in energy prices, which have risen substantially this year. The spikes have been particularly intense for fuel oil — which is used for industrial and domestic heating — and for crude oil, which directly translates to gasoline prices at the pump.

The United States faces a default sometime between Dec. 21 and Jan. 28 of next year if Congress does not act to raise or suspend the debt ceiling, the Bipartisan Policy Center warned on Friday.

The projection was a more narrow window than the nonpartisan think tank previously provided last month and the group suggested that the actual deadline, or X-date, could be in the earlier end of that range.

Democrats and Republicans appear to have tempered their tone around the latest debt limit standoff this time around, yet there is no current plan for lifting the borrowing cap. Republicans continue to insist that Democrats must act alone to address the issue, while Democrats have countered that raising the borrowing cap is a shared responsibility given that both political parties have incurred big debts over the last several years.

“Those who believe the debt limit can safely be pushed to the back of the December legislative pileup are misinformed,” said Shai Akabas, BPC’s director of economic policy. “Congress would be flirting with financial disaster if it leaves for the holiday recess without addressing the debt limit.”

Treasury Secretary Janet L. Yellen warned lawmakers in November that the United States could be unable to pay its bills soon after Dec. 15.

During testimony before the Senate Banking Committee this week, she underscored the urgency of the matter.

“I cannot overstate how critical it is that Congress address this issue,” Ms. Yellen said. “America must pay its bills on time and in full. If we do not, we will eviscerate our current recovery.”

After approaching the first default in American history, Congress in October raised the statutory debt limit by $480 billion, an amount the Treasury Department estimated would allow the government to continue borrowing through early December.

The Bipartisan Policy Center said that there is additional uncertainty surrounding the debt limit this year because of the pandemic and the various economic relief programs that are still ongoing.

Dec. 15 is particularly important because the Treasury Department is required to make a $118 billion payment to the Highway Trust Fund. If corporate tax receipts that are due that day come in weak, Treasury could face a cash crunch and the United States would be unable to fully meet all of its obligations like paying out Social Security and funding military paychecks.

The Congressional Budget Office said earlier this week that it expected that Treasury might run out of cash by the end of December if Congress fails to act. The C.B.O. suggested, however, that Treasury might be able to defer some Highway Trust Fund payments, which were mandated in the recently passed infrastructure law, potentially staving off a default until sometime in January.

Royal Dutch Shell said Thursday that it had decided not to invest in a British oil development off the coast of Scotland that has become a test of the government’s environmental credentials.

The field, known as Cambo, is in deep water northwest of the Shetland Islands. It is seen as a bellwether for the future of Britain’s declining but still large North Sea oil industry.

The British government is considering whether to approve the project, which environmental groups and some politicians have said should be rejected because it would produce carbon dioxide emissions responsible for climate change.

Shell, which owns 30 percent of Cambo, said it had “concluded the economic case for investment in this project is not strong enough at this time.”

The company also said there was “potential for delays,” apparently referring to the possibility that the drilling would draw protests from environmental groups and possibly legal actions trying to stop it. Shell said recently that it planned to move its headquarters from the Netherlands to Britain.

Shell’s decision to decline to invest in developing Cambo is a serious blow to the project. Siccar Point Energy, a private equity-backed firm that is Cambo’s main owner and developer, said that while “disappointed” by Shell’s decision, it remained “confident about the qualities” of the project, saying it would create 1,000 jobs.

Siccar Point has said that it plans to invest $2.6 billion in Cambo and that it has already spent $190 million in the four years since it acquired the rights to the field, which was discovered in 2002.

The oil industry argues that as long as Britain consumes more oil and natural gas than it produces, it is preferable for those fuels to come from the North Sea, where emissions regulations can be set, instead of from places with potentially fewer controls.

The environmental group Greenpeace UK said letting Cambo go ahead “would be a disaster for our climate and would leave the U.K. consumer vulnerable to volatile fossil fuel markets.”

Shareholders in BuzzFeed, the digital media pioneer known for its listicles, quizzes and a news division that won its first Pulitzer Prize this year, voted on Thursday to take the company public.

The deal that will take BuzzFeed onto the stock market raised less money than initially expected, which could crimp the company’s spending in the years to come and lead it to rein in its ambitions.

The long-in-the-works plan, led by the BuzzFeed co-founder and chief executive Jonah Peretti, will merge it with a special purpose acquisition company, 890 5th Avenue Partners. So-called SPACs raise money through an initial public offering and use that cash to buy a private company.

The deal is expected to close by Friday, 890 5th Avenue Partners said in a news release. BuzzFeed will make its stock market debut as soon as Monday, under the ticker symbol BZFD. Part of the deal includes the completion of BuzzFeed’s $300 million acquisition of Complex Networks, a sports and entertainment publisher.

Because investors who buy into a SPAC do not know what company it plans to buy, they have the opportunity to redeem those shares at their I.P.O. price — in this case $10 — before it reaches any deal. Many did. BuzzFeed could have raised over $250 million from the investors in the SPAC, but in the end it got only $16 million, according to a news release from BuzzFeed and 890. But BuzzFeed will have $150 million that it is raising from selling a debt security. Other SPAC deals in recent weeks have suffered from shareholders asking for their money back.

As the shareholders were casting their votes, a move that could mean millions of dollars for its early investors and some current and former staff members, not everyone at the company was cheering: Union employees at its news division, BuzzFeed News, staged a daylong work stoppage in an effort to speed contract negotiations. All 61 of the workers who belong to the BuzzFeed News Union, which includes reporters, editors and designers, took part, the union said.

In a statement, the union accused the company of refusing to budge in contract negotiations. The main sticking point is pay. The union said BuzzFeed was proposing a 1 percent guaranteed annual wage increase and a minimum salary of $50,000.

“We deserve a strong contract that protects us and ensures a fair and equitable workplace for everyone in our unit,” Katie Notopoulos, a senior tech reporter, said in the statement.

A BuzzFeed spokesman said the company would be back at the negotiating table “next Tuesday where we hope the union will present a response on these issues.”

The union, which formed in February 2019, is represented by the NewsGuild, which also represents workers at The New York Times and other media outlets. The union and the company have yet to agree on a first contract.

BuzzFeed was started out of a small office in New York’s Chinatown in 2006 as an experimental project in viral media for Mr. Peretti, back when his day job was chief technology officer of The Huffington Post. He devoted himself full time to BuzzFeed in 2011, after AOL bought HuffPost for $315 million, and transformed it into a stand-alone media company with the help of $35 million from investors.

It was soon hailed as the future of the news media. In recent years, though, it has missed revenue targets, and some investors pushed for a sale. Last year, BuzzFeed gained scale when it acquired HuffPost from its last owner, Verizon, in a stock deal.

Regulators in California said on Thursday that they had fined Pacific Gas & Electric $125 million for its role in causing the Kincade fire, which injured four people and destroyed hundreds of buildings in 2019.

As part of a settlement with the regulator, the California Public Utilities Commission, the company will pay the state $40 million and will forgo collecting $85 million it is entitled to from its customers in the state. The commission’s action followed a determination by investigators at the California Department of Forestry and Fire Protection that a PG&E transmission line caused the fire.

PG&E said it reached the settlement to more quickly compensate victims and so it could continue improving its systems, which have been responsible for many fires in recent years, including the deadliest one in state history, the 2018 Camp fire.

“We will continue our work to make it safe and make it right, both by resolving claims stemming from past fires and through our work to make our system safer,” PG&E said in a statement.

Regulators and the courts have ordered PG&E to pay hundreds of millions of dollars in fines for starting wildfires. The utility filed bankruptcy in January 2019 after amassing $30 billion in liability related to fires.

The Kincade fire burned almost 78,000 acres in Sonoma County over two weeks in October and November 2019.

Officials are investigating the company’s equipment in at least three fires that burned this year, including the Dixie fire, the second-largest wildfire in California history.