HONG KONG, Dec 3 (Reuters) – Just five months after its debut, ride-hailing giant Didi Global (DIDI.N) said it plans to withdraw from the New York Stock Exchange and pursue a Hong Kong listing, a stunning reversal as it bends to Chinese regulators angered by its U.S. IPO.

The company’s shares were down around 15% after swinging between gains and losses in premarket trading as investors initially bet the move would appease Beijing and serve as a catalyst for a revival of its business prospects at home.

“Following careful research, the company will immediately start delisting on the New York stock exchange and start preparations for listing in Hong Kong,” Didi said on its Twitter-like Weibo account on Friday.

Register now for FREE unlimited access to reuters.com

Register

Didi did not explain its reasons for the plan but said in a separate statement it would organise a shareholder vote at an appropriate time and ensure its New York-listed stock would be convertible into “freely tradable shares” on another internationally recognised stock exchange.

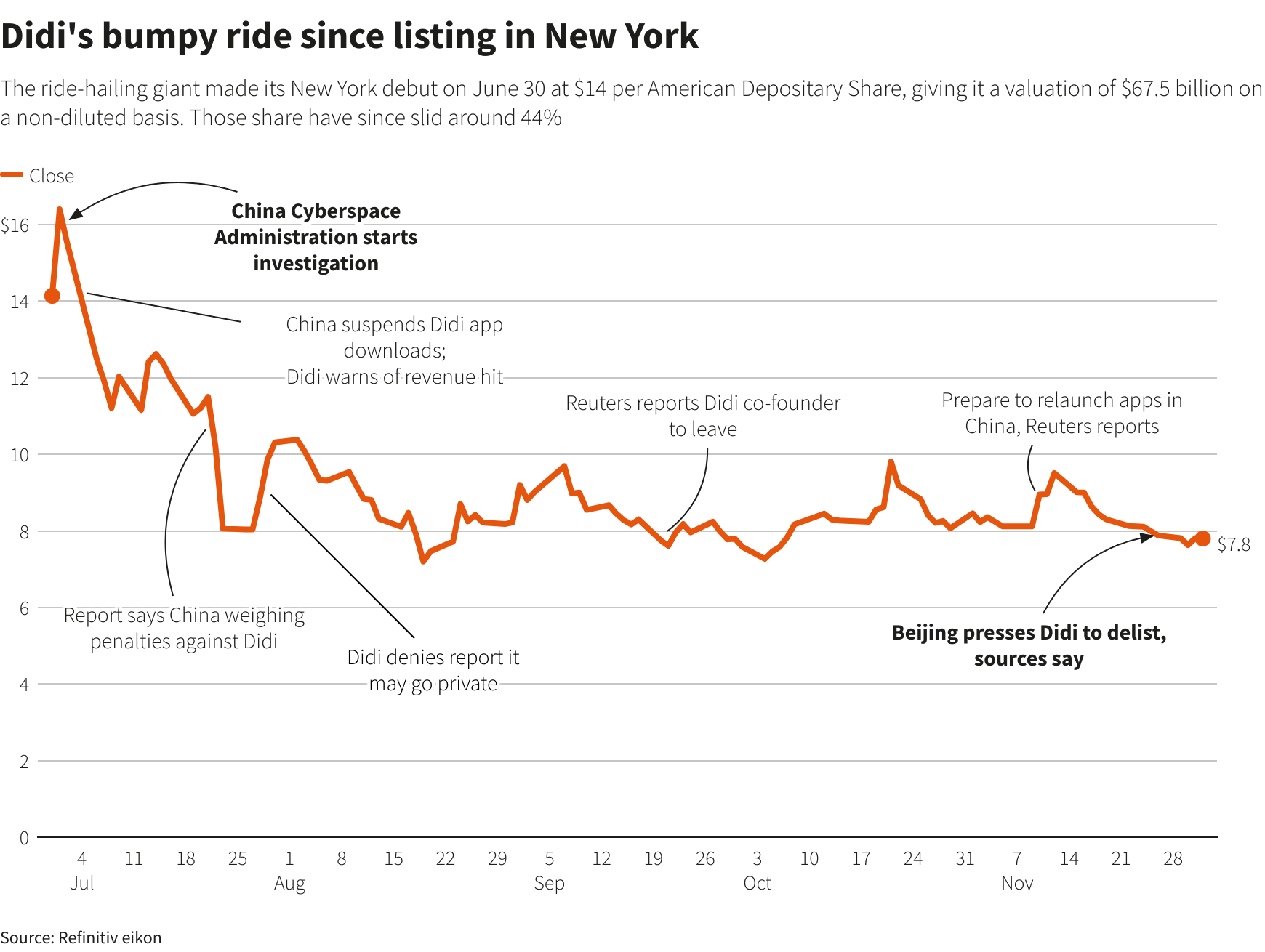

Sources told Reuters last month that Chinese regulators had pressed Didi’s top executives to devise a plan to delist from the New York Stock Exchange due to concerns about data security.

Didi’s board convened on Thursday and approved the U.S. delisting and HK listing plans, said two sources with knowledge of the matter.

Didi pushed ahead with a $4.4 billion U.S. initial public offering in June despite being asked to put it on hold while a review of its data practices was conducted.

The powerful Cyberspace Administration of China (CAC) then quickly ordered app stores to remove 25 of Didi’s mobile apps and told the company to stop registering new users, citing national security and the public interest.

Didi, whose apps, in addition to ride-hailing, offer products such as delivery and financial services, remains under investigation.

Redex Research analyst Kirk Boodry, who publishes on Smartkarma, said there is an expectation Didi may need to buy shares at the $14 IPO price to avoid legal issues and at the very least will pay more than the shares current trading price.

However, there was still uncertainty over what the delisting means for investors. “There may also be some hope that by doing this, Didi management will improve its regulatory relations, but I am less confident on that,” Boodry added.

The upending of Didi’s New York listing – likely to be a difficult and messy process – illustrates both the huge clout that Chinese regulators possess and their emboldened approach to wielding it.

Billionaire Jack Ma also ran afoul of Chinese authorities after blasting the country’s regulatory system, leading to the dramatic scuppering of a mega-IPO for Ant Group last year.

Did’s move will likely further discourage Chinese firms from listing in the United States and could prompt some to reconsider their status as U.S. publicly traded companies.

“Chinese ADRs face increasing regulatory challenges from both U.S. and Chinese authorities. For most companies, it will be like walking on eggshells trying to please both sides. Delisting will only make things simpler,” said Wang Qi, CEO at fund manager MegaTrust Investment (HK).

Didi is planning to proceed with a Hong Kong listing soon and is not looking at being taken private, sources with knowledge of the matter told Reuters.

It aims to complete a dual primary listing in Hong Kong in the next three months and delist from New York by June 2022, said one of the sources.

The sources were not authorised to talk to the media and declined to be identified. Didi did not immediately respond to Reuters’ requests for comment, and the CAC has yet to comment on its announcement.

“Not long after the IPO U.S. investors had been trying to sue DiDi for failing to disclose its ongoing talks with the Chinese authorities. This is unlikely to be taken any better,” said William Mileham, an equity analyst at Mirabaud. “It appears that DiDi are not waiting to be dual-listed, but could well be de-listed from the U.S. before it starts trading on the HK stock exchange.”

HONG KONG HURDLES

Listing in Hong Kong, however, might prove complicated, particularly in a tight three-month timeframe, given Didi’s history of compliance problems and the scrutiny it has faced over unlicensed vehicles and part-time drivers.

Only 20%-30% of Didi’s core ride-hailing business in China is fully compliant with regulations requiring three permits relating to the provision of ride-hailing services, vehicle licensing and drivers’ licences, sources have previously said.

Didi said in its IPO prospectus it had obtained ride-hailing permits for cities that collectively accounted for the majority of its total rides. It has not responded to further queries about permits.

Those problems had been the main obstacle to the company conducting an IPO in Hong Kong earlier and it remains to be seen whether the bourse will approve it now, sources with knowledge of the matter said on Friday.

“I don’t think Didi qualifies to be listed anywhere before it… sets up effective protocols to manage and ensure the drivers’ responsibility and benefits,” said Nan Li, associate professor for finance at Shanghai Jiao Tong University.

The Hong Kong bourse (0388.HK) does not comment on individual companies, a spokesperson said. Shares on the exchange however jumped 4% on prospects of a Didi listing.

Didi provided 25 million rides a day in China in the first quarter, according to its IPO prospectus. It made its New York debut on June 30 at $14 per American Depositary Share, but those shares had slid 44% by Thursday’s close, valuing it at $37.6 billion.

Its main shareholders are SoftBank’s Vision Fund, with a 21.5% stake, and Uber Technologies Inc (UBER.N), with 12.8%, according to a filing in June by Didi.

Sources have also told Reuters that Didi is preparing to relaunch its apps in China by the end of the year in anticipation that Beijing’s cybersecurity investigation of the company would be wrapped up by then.

Register now for FREE unlimited access to reuters.com

Register

Reporting by Julie Zhu, Kane Wu, Cheng Leng and Zoey Zhang; Additional reporting by Brenda Goh, Josh Horwitz, Alun John, Sayantani Ghosh, Scott Murdoch and Marc Jones; Editing by Sumeet Chatterjee, Edwina Gibbs, Jan Harvey and Dan Grebler

Our Standards: The Thomson Reuters Trust Principles.