People who experienced the Great Inflation are more likely to fear high inflation around the corner than the young, who have lived mostly in an era in which inflation has rarely exceeded 2 percent. The young’s experience of economic stagnation during their formative years, after the housing bubble burst in 2008, is more likely to convince them that inflation can be too low, as it was back then, stymieing efforts by the Fed to reinvigorate the economy.

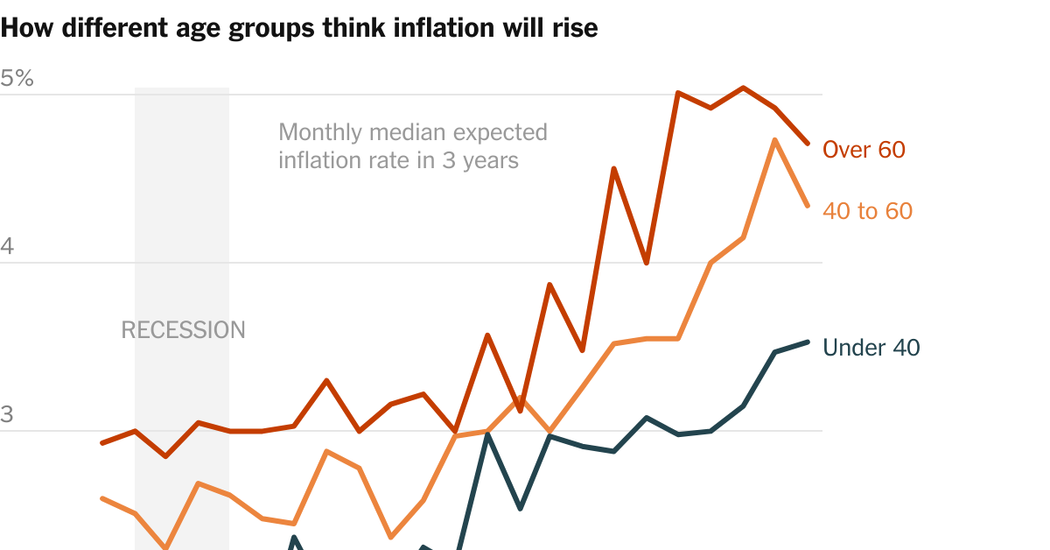

Americans under 40 expect inflation to hit about 3.5 percent in three years, according to the most recent reading of the New York Fed’s survey. People over 60, by contrast, expect 4.7 percent. “Younger and older people tend to differ depending on the path inflation took in their past,” Mr. Nagel said.

Even the experts — the members of the Federal Open Market Committee, the Fed’s policymaking group, who pore through sophisticated economic models fed with reams of data — are influenced by youthful memories. “Whether and at what age they experienced the Great Inflation or other inflation realizations affects their stated beliefs about future inflation, their monetary-policy decisions, and the tone of their speeches,” according to another paper by Ms. Malmendier, Mr. Nagel and Zhen Yan from Cornerstone Research in Boston.

The researchers do not have insight into the current view of committee members. Individual forecasts from the semiannual Monetary Policy Report to Congress, on which they based their analysis, are made available to the public only with a 10-year lag, starting in 1992. But their research helps explain a longstanding puzzle.

The puzzle came in a study by the economists David and Christina Romer of the University of California, Berkeley, in the middle of the last recession, in 2008. They found that over time, forecasts from the members of the Federal Open Market Committee were less accurate than the collective forecast of the staff economists at the Federal Reserve. The deviation, according to Ms. Malmendier, Mr. Nagel and Mr. Yan is “explained by reliance on personal inflation experiences.”

People not schooled in economics may have little clue about how inflation and monetary policy work. One study by economists at the Federal Reserve Bank of Cleveland; the University of California, Berkeley; the University of Texas at Austin, and Brandeis University found that the Fed’s momentous switch announced in August of last year to a flexible inflation target, which would allow the Fed to let inflation rise above its long-term target of 2 percent, was greeted by a collective “huh?”

Corporate executives do little better. “Like households, U.S. managers are largely uninformed about recent aggregate inflation dynamics or monetary policy,” wrote another group of economists in a separate study. “Inattention to inflation and monetary policy is pervasive among U.S. firms as well.”