Junk bonds are still in la-la-land though, Apocalypse but not now.

By Wolf Richter for WOLF STREET.

When investors demand higher yields on bonds, motivated sellers must lower the price of those bonds in order to sell them. And yields are now spiking and prices of bonds with longer maturities are plunging.

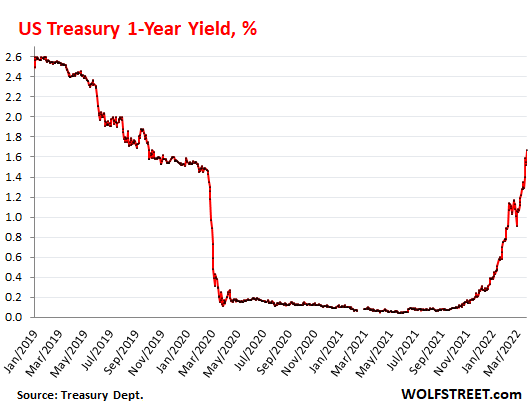

The one-year Treasury yield spiked by 38 basis points during the week, including 12 basis points on Friday, to 1.67%, the highest since October 2019. There is now a huge 150 basis point spread between the one-month yield of 0.17% and the one-year yield of 1.67%:

This is one heck of a fast-moving train. And the Fed hasn’t even done much other than one tiny rate hike and lots of talking about what it’s going to do, which is raise rates far faster and further than previously imagined, and kick off Quantitative Tightening “as soon as” May to finally crack down on inflation which is now spiraling out of control. And the credit markets got the memo.

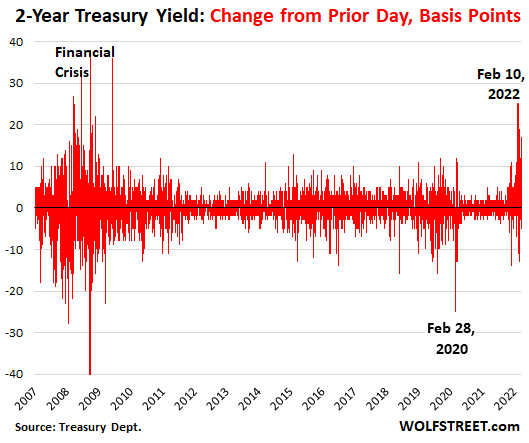

The two-year Treasury yield spiked by 33 basis point during the week, including a massive 17 basis points on Friday, to 2.51%, the highest since April 2019.

The volatility in the two-year yield is huge, the worst since the Financial Crisis, with massive spikes interrupted by some modest drops. This chart shows the day-to-day changes in the two-year yield in basis points. The biggest one-day spike in this cycle, 25 basis points, occurred on February 10:

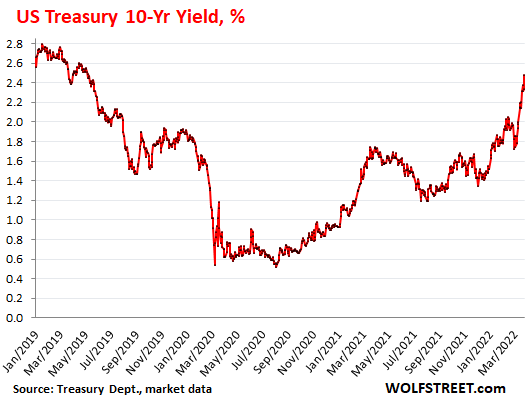

The 10-year Treasury yield spiked by 34 basis points during the week, including by 14 basis points on Friday, to 2.48%, the highest since May 2019.

The 10-year yield has been rising since the low point of 0.52% on August 4, 2020, which marked the top of the biggest bond bull market ever that had started in October 1981. At the time, the 10-year yield had peaked at 15.8%, after CPI inflation had peaked in April 1980 at 14.6%.

From October 1981, yields zigzagged lower, interrupted by big upticks in between, and since 2008 pushed down by the Fed’s interest rate repression and massive QE. Now the result is the highest inflation since 1981, with February CPI at 7.9% and worse inflation to come.

The bond massacre in dollars. Market prices of bonds with long remaining maturities get ravaged when interest rate rise.

For example, the price of the iShares 20 Plus Year Treasury Bond ETF, which holds Treasuries with maturities of 20 years and longer, fell 1.4% on Friday to $128.66. This was down 25% from the peak at the end of July 2020. The 40 years of bond bull market have lulled people to sleep about the risks of bond funds.

But not junk bonds yet. This massacre is playing out with Treasury securities and with investment-grade corporate bonds, particularly the highest-rated corporate bonds that closely track Treasury securities.

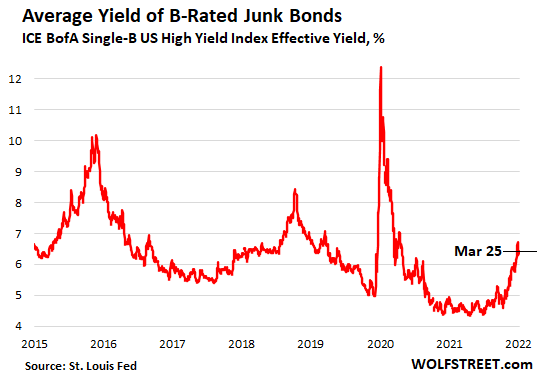

Junk bond yields have been slowly rising from the low point last summer, and the spreads to Treasuries have been slowly widening. But since March 15, while all heck broke loose in the Treasury market, junk bond yields have actually dropped and remain historically low, and their spreads have narrowed and are historically narrow.

This means that the market is still not paying attention to corporate credit risk – the risk of default – and the market is still chasing yield and is still giving these junk-rated companies with a significant probability of default a pass on credit risks, which is going to haunt the market when it wakes up. Apocalypse but not now.

This chart shows the average yield of B-rated high-yield bonds. A “B” rating is roughly mid-range within the junk bond spectrum (here’s my cheat sheet for corporate bond credit ratings and what they mean in plain English):

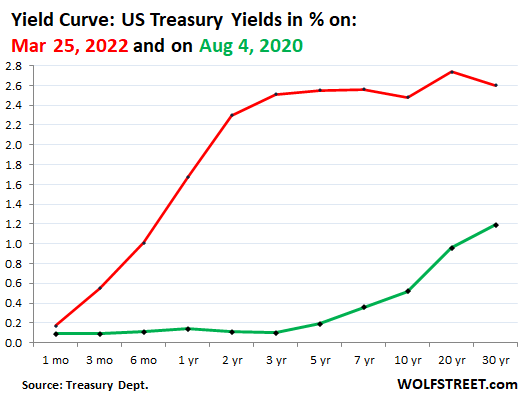

The yield curve is now very steep from the one-month yield (0.17%) through the three-year yield (2.51%). But then it flattens through the seven-year yield, inverts a tiny bit at the 10-year yield, then steepens to the 20-year yield, and then inverts again to the 30-year yield.

The yield curve still says nothing about the economy because it is still an artificial construct manipulated by the Fed: The Fed still represses the short end of the yield curve with its policy interest rates, and its obese balance sheet sits on top and squishes the long end of the yield curve. At some point QT, once it reaches critical mass, is going to start freeing the long end of the yield curve, and long-term yields will rise much further, the curve will steepen at the long end.

The chart also shows the yield curve on August 4, 2020 (green), marking the end of the 40-year bond bull market, to be cut out and taped on the fridge with a melancholic nostalgic smile:

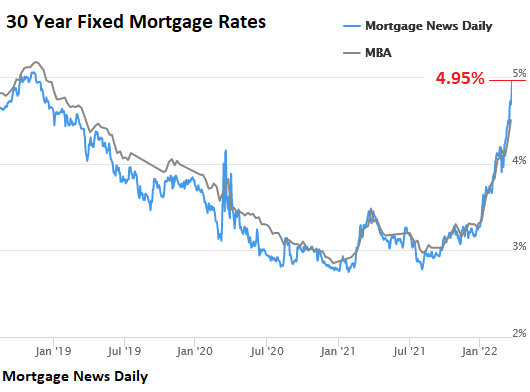

Mortgage rates, holy moly. On Friday, the average 30-year fixed mortgage rate spiked to 4.95%, the highest since November 2018, according to Mortgage Daily News. And once it goes over 5.15%, it would be the highest since before the Financial Crisis. But back then, and back in 2018, home prices were a lot, lot lower. Already, layer after layer of buyers are stepping away from the market at these mortgage rates:

But as the WOLF STREET dictum goes, “nothing goes to heck in a straight line.” It is very likely that Treasury yields will pull back some, after this run-up. And hedge funds that are short Treasuries – the most obvious no-brainer in the history of mankind – are going to get whacked around. That’s always how it is. One thing we know: it’s going to be volatile, with massive moves in both directions. And the 5% mortgage rate is sort of the sound barrier, and it will take a while to move beyond it in a significant way. But its impact on the housing market is already being felt.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()