Traders work on the floor of the New York Stock Exchange (NYSE) in New York City, U.S., March 29, 2022. REUTERS/Brendan McDermid

Register now for FREE unlimited access to Reuters.com

NEW YORK/LONDON, March 29 (Reuters) – World share markets surged and global borrowing costs climbed on Tuesday, as the first face-to-face talks between warring Russia and Ukraine in nearly three weeks yielded signs of progress. read more

U.S. stock indices jumped over 0.5%, Europe’s main bourses enjoyed 1% to 2.5% gains, and oil tumbled 4% as Russia’s deputy defence minister emerged saying Moscow has decided to drastically cut military activity around Ukraine’s capital Kyiv and also Chernihiv. read more

Wall Street looked set to extend a three-day run of gains. Asia had been lifted overnight too after the Bank of Japan defended its vast stimulus programme, although the yen’s worst month since 2016 was still raising eyebrows. /FRX

Register now for FREE unlimited access to Reuters.com

Dealers also shrugged off bigger-than-expected drops in French and German consumer confidence data and signs that Russia will push ahead with plans to start billing for its gas in roubles, and is prepared to risk a historic sovereign debt default. read more

Germany’s benchmark 10-year Bund yield – the main gauge of European borrowing costs – hit its highest since early 2018 and 2-year yields turned positive for the first time since 2014, adding to the seismic shifts in global rates markets this year as inflation has surged.

U.S. Treasury yields paused their ascent on Tuesday, but have risen an eyewatering 165 basis points this quarter.

Benchmark 10-year U.S Treasuries were at 2.426% while the equivalent 2-year yields were at 2.38%, More than 200 basis points of U.S. interest rate rises are also now priced in for 2022 which, if realised, would be the most in a calendar year since 1994.

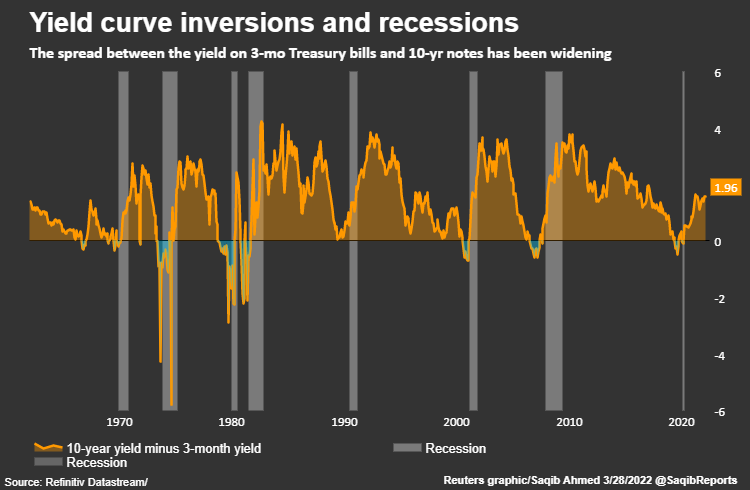

The difference between 2- and 10-year Treasury yields seems well on the way to turning negative for the first time since 2019 as well.

This is the so-called curve inversion that is considered a reliable predictor of recession, although the U.S. Federal Reserve has urged investors to also watch other curve segments which are still steep, giving it room to tighten policy further and faster.

“We have seen something that is a little unprecedented because the Fed is suddenly facing a question about its credibility and whether it can effectively reduce inflation,” said Amundi’s head of multi-asset strategies, Francesco Sandrini.

He added that Amundi had revised its European growth forecast downward to 1.5% for the year from 2% previously, but it could be lower if the situation continues to deteriorate.

“We question a lot our forecasts,” Sandrini said, especially as Europe’s big companies are more heavily exposed to commodity price pressures than U.S. counterparts. “It is extremely complicated, we need to proceed cautiously.”

BATTERED YEN

The Dow Jones Industrial Average (.DJI) rose 0.59%, the S&P 500 (.SPX) gained 0.50%, and the Nasdaq Composite (.IXIC) climbed 0.73%. MSCI’s gauge of stocks across the globe (.MIWD00000PUS) gained 1.03%.

All the three of the main S&P 500, Dow Jones and Nasdaq indexes are on course to end March higher. However, they are also set to record their worst start to a year and indeed any quarter since the start of 2020 when the outbreak of the coronavirus pandemic wreaked havoc on financial markets.

Japanese shares (.N225) had closed up more than 1% in Asia overnight although Chinese stocks and oil both slid as Shanghai continued to lock down to combat a COVID-19 surge.

Tokyo’s rally had come as the Bank of Japan vowed to keep its stimulus pumping, offering to buy unlimited amounts of 10-year government bonds to prevent its bond yields from rising too much further.

The central bank was finding it tough going, however. The 10-year JGB yield stood at 0.245%, right up against the BOJ’s implicit 0.25% cap.

This didn’t help the yen much, which was at 122.54 per dollar even after staging a small recovery from its bruising the day before.

“Excess volatility and disorderly currency moves could hurt economic and financial stability,” Japan’s top currency diplomat Masato Kanda told reporters on Tuesday, confirming the resolve of Japan and the United States to closely communicate on exchange-rate issues.

Elsewhere, trading remained choppy. Investors will favour markets that are lagging the Fed’s rate hike, operating on “a day-to-day trading mentality” amid market noise and short-term developments, said Chi Lo, senior market strategist APAC at BNP Paribas Asset Management.

“There is not really even medium-term direction that the market is following,” he said.

Among commodities, oil prices saw another sudden $4 plunge as Russia’s top negotiator in the Ukraine talks described the discussions as “constructive”. That left Brent down 3.8% at $108.22 per barrel and U.S. WTI at $102.04.

Prices had weakened earlier too as China’s financial hub Shanghai tightened its latest COVID-19 lockdown, after it reported a record 4,381 asymptomatic cases and 96 symptomatic cases for March 28 – though the caseload remains modest by global standards. read more

“Certainly commodity markets will not be comfortable in the short term with China shutting down,” Lo said. Many observers estimate less than 5% growth this year for the world’s second-biggest economy, he said, a view he rated as “too pessimistic” given expectations for stronger stimulus measures.

Spot gold dropped 0.8% to $1,907.08 an ounce.

Register now for FREE unlimited access to Reuters.com

Additional reporting by Selena Li in Hong Kong, Editing by Ed Osmond, Andrea Ricci and Jonathan Oatis

Our Standards: The Thomson Reuters Trust Principles.