(Bloomberg) — The U.S. went on a borrowing binge last year and the hangover could make it harder for the Federal Reserve to fight inflation without crashing the economy.

Most Read from Bloomberg

Corporate debt has surged $1.3 trillion since the start of 2020 as borrowers took advantage of emergency Fed action as the pandemic spread, slashing interest rates and backstopping financial markets to keep credit flowing. More debt held by more companies suggests potential risks as borrowing costs rise from currently low levels.

That could create financial stability concerns for Fed Chair Jerome Powell and his colleagues as they debate removing pandemic support in the face of what a report Friday showed were the hottest price rises in almost 40 years. And a tough task: Not since Alan Greenspan’s time has the U.S. central bank tried to navigate the economy back to price stability from too-high inflation.

Powell’s challenge is to try to curb price pressures without large costs to employment or growth, a move that would likely anger both political parties and blotch his record with the first Fed-assisted hard landing since the 1990-1991 downturn.

“They are in a difficult position,” said Jeremy Stein, professor of economics at Harvard University and a Fed governor from 2012 to 2014. If inflation is more persistent “and they really have to hike rates significantly, you can imagine what happens to asset valuations: There’s just a tremendous amount of interest-rate sensitivity in markets.”

The Fed’s Financial Stability Report on Nov. 2 noted that key measures of vulnerability from business debt, including leverage and interest cover ratios, were back at pre-pandemic levels.

But it also discussed risks to asset prices from a sharp rise in interest rates that could slow growth and lead to harmful losses.

Intense market volatility has swayed the Powell Fed before. Officials paused after raising rates in late 2018 in the face of severe swings in stocks and bonds and cut rates three times the following year.

Financial stability remains on policy makers’ minds. Minutes of their November meeting show that a number of them raised it during their deliberations, as they decided to start scaling back bond buying.

Powell said last week that officials would consider accelerating their reduction of asset purchases when they meet Dec. 14-15 to end the program a few months earlier than mid-2022, as initially planned.

Wrapping the taper up sooner gives the Fed scope to raise rates earlier and faster if inflation fails to ease next year as expected. But record levels of debt may force them to temper their actions.

More Slowly

“They may move a little bit more slowly to see how things develop, and whether problems do come up in the U.S. — at least in the non-financial corporate business sector,” said William English, professor at Yale School of Management and a former senior Fed economist. “That will be just another source of uncertainty for monetary policy.”

The Fed’s emergency response to the pandemic included unprecedented support for the corporate sector. And while the intervention wasn’t massive compared to some of the Fed’s pandemic programs, the backstop fueled a record borrowing surge at historically low rates.

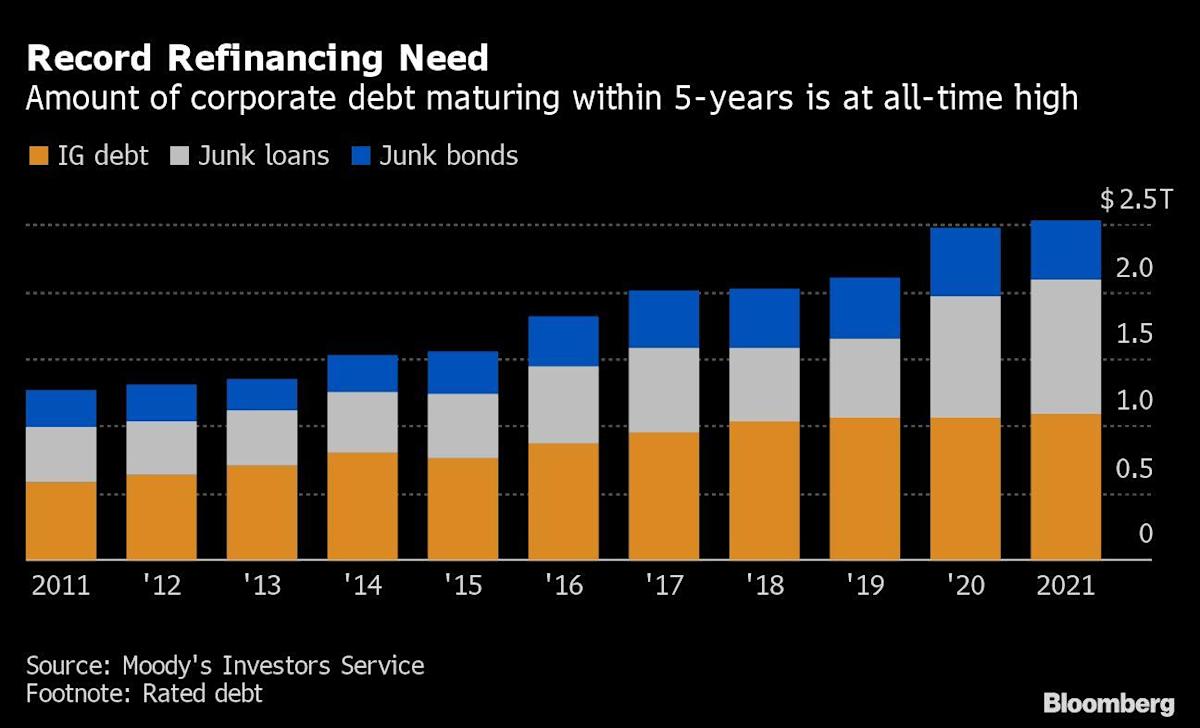

The combination has pushed investment-grade bond duration, the so-called sensitivity to interest rates, to near-records and boosted five-year refinancing requirements to all-time highs of around $2.5 trillion, according to Moody’s Investors Service.

If higher rates and wider corporate borrowing spreads throttle access to credit, it could push more firms into bankruptcy.

“There are negative aspects when you encourage people to borrow, but then later feel that you can’t raise rates because so many people borrowed,” said Howard Marks, co-founder of Oaktree Capital Group. “That’s something of a trap.”

To be sure, big firms that used the opportunity to issue longer-dated bonds at lower rates have strengthened their balance sheets.

Higher corporate profits would also ease the strain, though these could come under pressure if the economy slows in response to tighter monetary policy.

But while many firms took advantage of the low rates, it wasn’t universal. Nearly 500 companies are expected to try to tap markets to refinance next year, according to S&P Global Ratings. Medium and small-sized firms whose loans don’t tend to be rated would struggle even more, according to Fitch Ratings.

Government and household debt also surged during the pandemic. While those segments look relatively healthy, rising borrowing costs could make servicing the federal debt more politically fraught and pressure lower-income Americans.

Some see the higher debt burden limiting how far the Fed will be able to raise rates.

“Financial conditions are relatively sensitive to what the Fed does. And the pandemic potentially made them more sensitive because we have seen debt increase,” said Tiffany Wilding, an economist at Pacific Investment Management Co. “That would suggest to us that probably the top of this hiking cycle, the terminal rate of this hiking cycle, could even be less than what it was in the last cycle.”

Corporate America also includes a number of weaker companies –- sometimes called zombie firms because they don’t generate enough cashflow to service their debt payments — which could be vulnerable as borrowing costs head back up.

Their number jumped during the pandemic to 772 among the publicly-traded firms in the Russell 3000, according to data compiled by Bloomberg. While the tally has shrunk to 621, there are still more than an additional 100 of them compared to before the pandemic.

In addition, the average credit rating of companies has been declining, according to Moody’s — an early warning that some of them could run into problems with paying what they owe if debt service costs rise.

“The economy is more vulnerable than it has ever been before to rising interest rates,” said Torsten Slok, chief economist at Apollo Global Management. “How much can the Fed raise rates? And the answer is, they can actually not raise rates that much.”

Most Read from Bloomberg Businessweek

©2021 Bloomberg L.P.